Is Buying a Home Now Better Than Six Months Ago?

/Carter Campbell with Houzd Mortgage is here to discuss if purchasing a home today is better than it was six months ago.

Believe it or not, today is a better time to buy a house than March of this year.

We did some research and in one scenario if you would have bought a house in March, it would have cost $550,000 with a rate of 5.5%. Resulting in a principal and interest payment of around $2,966.

Also, let’s not forget the other difficulties that came from purchasing six months ago. You would have had to overbid on the home to even get your offer accepted, seller concessions were unheard of, and there were barely any homes to choose from. You probably would have been counting your blessings that you got your offer accepted.

Today the power has shifted back to the buyers. You can offer lower than list price, there are more homes to choose from, and sellers themselves are even advertising that they are willing to pay closing costs and a 2-1 Buydown fee.

So, if you bought the same house today, you could purchase it for $480,000. If the seller were to pay the 2-1 Buydown fee the monthly payments become very affordable.

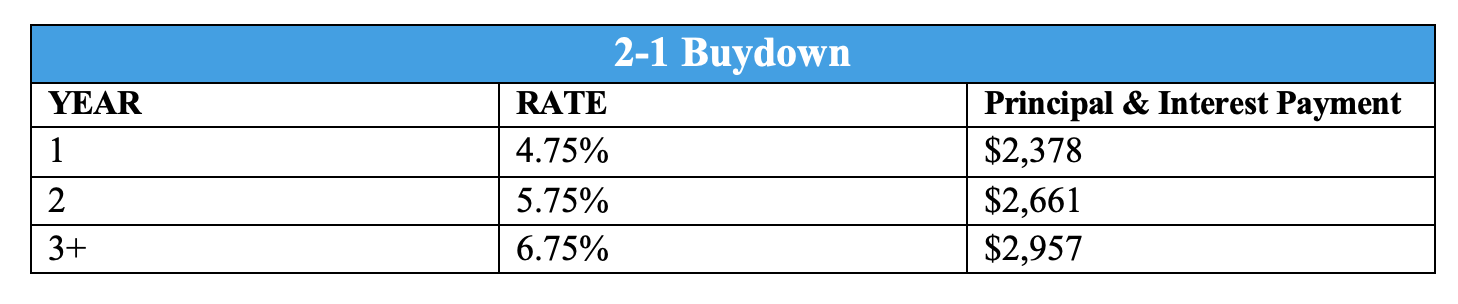

Your rate would start at 4.75% which would make your monthly principal and interest payment $2,378 for year one. Year two your rate would move to 5.75% with a payment of $2,661, and in year three your rate would make its final move to 6.75% and your payment would be $2,957.

The great news is this will be the highest payment your home will ever be. It will only go down from here. We don’t believe rates will stay this high forever and our expectation is that within 18 months rates will drop to around 4.5%. If you were to purchase a house today at the $480,000 and within 18 months, we can refinance you to 4.5% rate your principal and interest payment would drop to $2,310.

Despite the current market conditions, there are still many buying opportunities available for those who are willing to act. By taking advantage of seller concessions and interest rate buydowns, you can secure a new home for a great deal. Moreover, if rates fall in the future, your payment will be even lower. So don't wait any longer – reach out to us today and let’s start reviewing your options for purchasing!

Seller Paid Interest Rate Buydown

The market has changed a lot in the last few weeks. Interest rates have gone up drastically. Home prices have begun to come down a little bit. Monthly payments are higher than they have been.

For buyers there is less competition which means there are more opportunities and more options to choose from. However, with rising rates many people think that buying a home is out of their reach, but this doesn't have to be the case.

The dilemma is finding the right financing strategy to make purchasing still affordable for you despite rising interest rates.

A recent approach we recommend for our clients to use, is negotiating with sellers to pay seller concessions to buydown the interest rate and pay for some of the buyer’s closing costs. This means that buyers can have a lower interest rate and monthly payment, making homeownership more affordable. And the best part is it is paid by the seller, so it doesn’t cost the buyers anything.

Asking for a large seller concession to buydown the interest rate about 1.25 - 1.5% lower, in most instances is saving buyers $500 per month.

For example, we could take someone with an interest rate of 6.5% and probably get them down to 5.25% by getting the seller to pay the amount for the buydown of the rate.

This makes the new monthly payment much more affordable right now!

If you are concerned about buying a new house, or monthly payments and interest rates being too high, our seller paid interest rate buydown strategy might be perfect for you.

How Much Can You Save With a 2-1 Buydown?

Are you qualified to buy a house this year, but your projected monthly payment is not where you want it to be? Don’t throw in the towel just yet!

It may be time to consider a 2-1 Buydown.

The 2-1 Buydown programs lowers the interest rate 2% for the first year and then 1% for the second year of your loan. The third and every year after has the regular payment.

This program is perfect for buyers who have the means to purchase but want a more affordable monthly payments in light of recent high interest rates. A 2-1 Buydown is available for all qualified home buyers and can be used in conjunction with other government programs, such as the First-Time Home Buyers Program.

Here is what the payments could look like using the 2-1 Buydown:

This program does come at a cost. For the example above with a $480,000 purchase price the cost would be around $7,000.

What sometimes works out nice is negotiating for the seller to pay this cost for you.

Back in covid times it was extremely rare for a seller to pay closing costs, but with where we are at in the market today, we are seeing it happen more and more. Sellers would rather pay a buyer’s closing costs than have to drop their listing price by $20,000.

With the 2-1 Buydown you can enjoy a lower payment for two years. But the goal is to ultimately refinance into lower rate before the regular payment takes effect. If the market cooperates and you are able to refinance, then you will have a lower payment today and a lower payment in the future.

If the opportunity to refinance doesn’t present itself, you have two years to prepare for the higher payment and a lot can happen in that time such as a job promotion or higher income.

If you are interested in seeing if the seller can pay for a 2-1 Buydown for you and what the payments would be, please reach out and we can run some numbers for you.